The OFAC 50 Percent Rule is the load-bearing wall of U.S. sanctions enforcement against Russia. It is also the line that the most sophisticated evasion structures are designed to sit just below. Using only public records — OFAC press releases, Treasury filings, ICIJ leak databases, court documents, and corporate registries — this briefing reconstructs how documented evasion structures actually work, where regulators draw their lines, and what an OSINT-grade ownership analysis looks like in practice.

TL;DR

The 50 Percent Rule says an entity is automatically blocked when blocked persons own 50% or more, directly or indirectly, in the aggregate. It does not, by its own text, capture control without ownership, and it depends on a counterparty being able to count what they cannot see. Three documented cases — Kerimov / Heritage Trust (2022), Deripaska / EN+ Group (2019), and GVA Capital (2025) — show how trust structures, sub-50% restructurings, and proxy holdings have been used to sit below the threshold. OFAC's 2025 enforcement against GVA Capital signals a shift toward control-based liability that compliance teams have not yet fully absorbed. This briefing documents the methodology we use to reconstruct ownership chains from open sources before the regulator sends a notice.

Why this matters

Sanctions screening tools answer a binary question: is the name on a list? The 50 Percent Rule is what makes that binary inadequate. Under OFAC FAQ 401, an entity in which one or more blocked persons hold an aggregate ownership interest of 50 percent or more — directly or indirectly — is itself blocked, even if it never appears on the SDN list.[1] That entity is invisible to a name-match screen. It will pass commercial KYC. It will pass automated sanctions software. The only way to detect it is to reconstruct the ownership chain from primary sources.

This is not theoretical. In June 2022, the U.S. Treasury Department issued a Notification of Blocked Property to Heritage Trust, a Delaware trust holding more than $1 billion in assets in which sanctioned Russian oligarch Suleyman Kerimov held an interest. Kerimov had been on the SDN list since April 2018.[2] The trust had been holding assets for more than four years before Treasury formally blocked them. During that window, U.S. financial institutions, asset managers, and counterparties had no automated way to know they were dealing with sanctioned property.

That is the structural problem this briefing addresses. The 50 Percent Rule is not a screening rule. It is an investigation rule. And the investigation is on the counterparty — not the regulator.

What the rule actually says (and what it does not)

The text matters. OFAC's revised 2014 guidance, restated in FAQs 398–402, establishes four operational principles:[3]

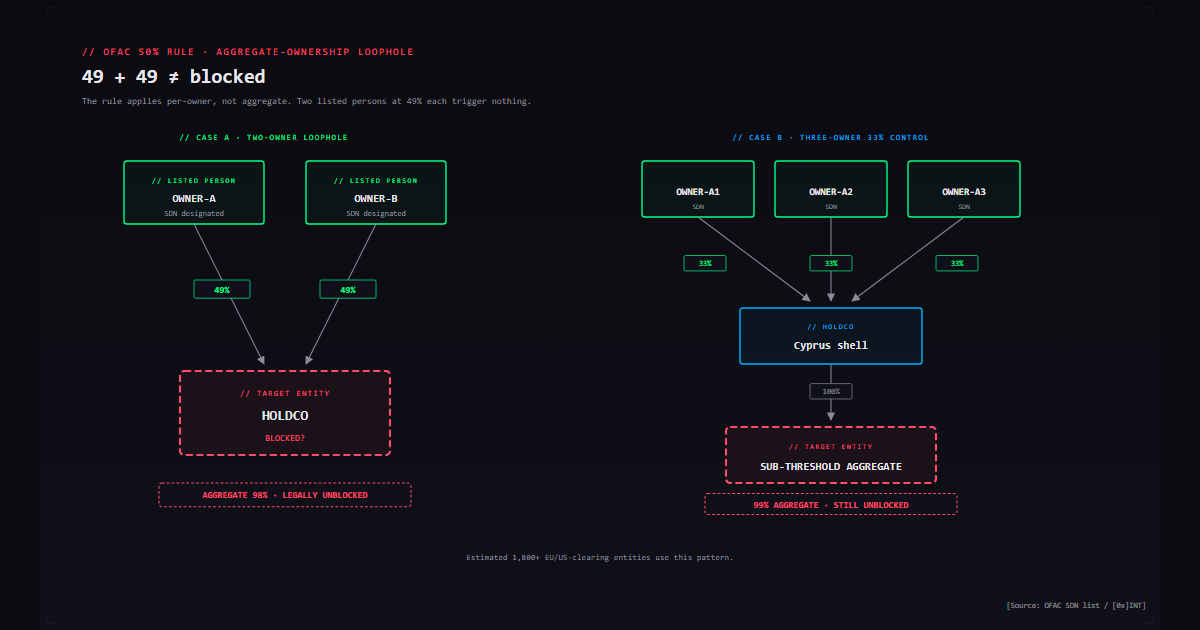

- Aggregation. If Blocked Person X owns 25% of Entity A and Blocked Person Y owns another 25%, Entity A is blocked. Ownership interests held by persons sanctioned under different OFAC programs are aggregated.

- Indirect ownership. Ownership through intermediate entities counts — but only when the blocked person owns 50% or more of the intermediate. A 49% stake in an intermediary that owns 100% of a target does not, on the face of the rule, make the target blocked.

- Ownership, not control. FAQ 401 explicitly states that "OFAC's 50 Percent Rule speaks only to ownership and not to control." An entity that is controlled but not owned 50% or more by blocked persons is not automatically blocked.

- Divestment. Per FAQ 402, if blocked persons reduce their combined ownership below 50%, the entity is no longer automatically blocked, provided the divestment occurs entirely outside U.S. jurisdiction and without U.S. persons.[4]

Each of these principles has been turned into a structuring opportunity. The next sections walk through three documented cases that illustrate how.

Case 1: The 45/45/10 split — Deripaska, EN+, and the price of staying out

Oleg Deripaska was added to the SDN list on 6 April 2018 alongside his principal corporate vehicles, including EN+ Group plc and UC Rusal. By that date Deripaska held approximately 70% of EN+, which in turn held a controlling interest in Rusal. Under the 50 Percent Rule, both EN+ and Rusal were automatically blocked through Deripaska's holding, and OFAC named them on the SDN list directly.[5]

What happened next is the cleanest public example of how the rule's threshold drives corporate restructuring. To obtain delisting of EN+ and Rusal — while Deripaska himself remained sanctioned — the parties negotiated a restructuring under which Deripaska's stake in EN+ was reduced from approximately 70% to 44.95%.[6] The 25 percentage points he gave up were redistributed: a portion to a charitable trust, a portion to VTB Bank (Russian state-owned), and a portion to Glencore. OFAC announced its intent to delist EN+, Rusal, and EuroSibEnergo in December 2018, and the delisting took effect in January 2019.

Two observations are essential. First, 44.95% was not a coincidence. It was engineered to sit below the 50% threshold while preserving as much of the original economic interest as possible. Second, the restructuring was accompanied by control safeguards that OFAC required as conditions of delisting — voting trust arrangements, board composition requirements, and reporting obligations — precisely because OFAC understood that ownership reduction alone did not eliminate Deripaska's influence.[7]

This is the regulatory tell. When OFAC has to negotiate control safeguards as a condition of delisting, it is implicitly acknowledging that the 50 Percent Rule, applied mechanically, undercounts influence. The Deripaska case is the most public articulation of that gap.

We cannot independently confirm the precise economic terms of the trust arrangements that hold the residual 25 percentage points, nor the voting and dividend rights attached to those stakes. These terms have been described in regulatory filings and press reporting but have not, to our knowledge, been published in full.

Case 2: Heritage Trust — what the rule misses when there is no public ownership chart

The Kerimov case is the inverse of Deripaska. Where Deripaska's holdings were public, listed-company stakes that could be restructured visibly, Kerimov's U.S.-facing assets were held through a private Delaware trust whose beneficial ownership was, by design, not on any registry.

The Treasury press release of 30 June 2022 sets out what was found:[8]

- Heritage Trust was formed in July 2017 to hold and manage Kerimov's U.S.-based assets.

- Kerimov was designated under E.O. 13661 in April 2018.

- Kerimov's interest in Heritage Trust was obscured through a "complex series of legal structures and front persons."

- Funds entered the U.S. financial system through two foreign Kerimov-controlled entities prior to his designation.

- Various layers of U.S. and non-U.S. shell companies held formal title to assets.

For more than four years — from Kerimov's April 2018 designation to Treasury's June 2022 notification — Heritage Trust held in excess of $1 billion in U.S. assets without being blocked. The trust was not on the SDN list. The shell companies holding formal title were not on the SDN list. Counterparties dealing with those shells had no automated signal that they were transacting with blocked property.

What changed in 2022 was not the underlying ownership. What changed was that Treasury investigators reconstructed the chain. The published source material does not specify which open-source records contributed to that reconstruction, but the elements that are typically available in cases of this type include:

- Delaware Division of Corporations records identifying the registered agent and date of formation;

- Real-property records (county recorder filings) identifying assets held by named LLCs;

- UCC-1 financing statements identifying secured creditors and collateral;

- SEC filings (Form D, beneficial ownership reports) where any of the underlying entities engaged with regulated funds;

- Corporate registry data for foreign holding entities — particularly Cyprus, BVI, and the Channel Islands — which Russian wealth structures have historically used as upper-tier vehicles.[9]

The Kerimov case demonstrates the rule's blind spot in the absence of a published ownership chart. When the upper-tier entities are private, when title is held through nominee LLCs, and when the relevant trust deeds are not public, a counterparty cannot perform the 50% calculation. They are dependent on whatever the trustees and front persons disclose. If those parties under-disclose — deliberately or otherwise — the counterparty inherits the regulatory risk.

The Polyus Gold transfer is a related data point. In 2015, Suleyman Kerimov reportedly transferred his Polyus Gold stake to his son Said Kerimov.[10] Said was added to the EU sanctions list in April 2022 and to the U.S. SDN list later in 2022. The intra-family transfer pre-dated either sanctions designation by seven years. The OFAC ownership analysis on Polyus during the period 2015–2022 would have turned on whether Suleyman Kerimov retained any beneficial interest after the transfer — a question that, again, depends on private documents not visible to ordinary counterparties.

We do not assert that any specific Polyus Gold counterparty failed to identify a blocked-property risk. The point is structural: the rule's application to intra-family transfers depends on facts that are typically not publicly disclosed.

Case 3: GVA Capital — the 2025 control-based pivot

If Deripaska shows the rule being engineered around, and Kerimov shows the rule being defeated by opacity, the GVA Capital enforcement of 2025 shows OFAC pushing back.

On the public record, GVA Capital Ltd. was assessed a penalty of $215.99 million in 2025 in connection with managing U.S. investments linked to a sanctioned Russian oligarch. The case has been described in legal commentary as accounting for approximately 81% of total OFAC penalties for 2025.[11] What is significant for our purposes is the legal theory.

In its enforcement narrative, OFAC declined to credit a "narrow, technical reading" of the 50 Percent Rule and focused instead on the firm's actual knowledge that the underlying oligarch retained a beneficial interest in and exerted control over the assets. Outside counsel for one of the involved parties (IPI) had earlier advised, on the basis of incomplete information, that blocking was not required under the 50 Percent Rule.[12]

The legal-practitioner commentary on this enforcement is consistent: OFAC is signalling that compliance obligations extend beyond formal corporate boundaries, and that structuring arrangements to evade or avoid sanctions can produce liability even where the formal ownership numbers are below 50%.[13] This is functionally a control-based interpretation operating alongside the formal ownership rule.

For compliance teams, the practical implication is that "below 50%" is no longer a safe harbour where actual control or beneficial interest can be inferred. The implication for OSINT analysis is that ownership reconstruction must now be paired with control reconstruction — voting agreements, board composition, signatory authority, fund-flow patterns — and that the relevant evidence base extends beyond corporate registries.

The structural patterns that repeat

Across the documented cases and the broader pattern of Russian wealth structuring revealed by the Pandora Papers, four design choices recur. We treat them as structural indicators — not as proof of evasion, but as factors that materially raise the prior probability that a deeper investigation is warranted.

Pattern A: Ownership clustered just below 50% with related-party residual

The clearest signal. A target entity in which a sanctioned person or close associate holds 45–49.99%, with the residual held by individuals or entities linked to the same family, business associates, or jurisdictionally co-located vehicles. The Deripaska 44.95% structure is the public template; variants appear in private structures whenever a known UBO needs to step formally below the line.

Pattern B: Trust or foundation interposition

A trust (often Delaware, Liechtenstein, Jersey, or Cyprus) interposed between the natural-person UBO and the operating assets. Trust deeds are typically private. Without them, a counterparty cannot determine whether the settlor retains effective beneficial ownership. Heritage Trust is the canonical example; the Pandora Papers documented hundreds of similar structures linked to Russian beneficial owners through service providers including Alcogal and Demetriades LLC.[14]

Pattern C: Pre-designation intra-family transfer

Transfer of significant holdings to a close relative (typically adult child) prior to any anticipated designation. Polyus / Said Kerimov is the documented example, though we note the transfer in that case occurred years before sanctions and we do not impute intent. The pattern matters for analysis: when an entity's ownership structure shows a family transfer occurring within 24 months of a sanctions risk event — e.g., Crimea annexation in 2014, full-scale invasion in 2022 — the timing is itself an investigative lead.

Pattern D: Multi-jurisdictional layering with aligned counsel

The Pandora Papers data shows that Russian beneficial owners cluster heavily around a small number of corporate-services providers, particularly in Cyprus and the BVI. The ICIJ found that Russian nationals were linked to nearly 3,700 entities in the Pandora Papers data — the largest national grouping in the dataset.[15] Many of those entities share registered agents, directors, and addresses. When an investigation surfaces a company whose Cyprus or BVI parent shares a registered agent with companies known to be linked to designated persons, that proximity is a material factor.

Methodology: how to reconstruct ownership from open sources

The following workflow is what we apply in practice. None of it requires private data. All of it requires patience, language coverage, and cross-referencing discipline.

Step 1 — Establish the formal ownership baseline

- For Russian operating entities: full EGRUL extract via the FNS portal (egrul.nalog.ru), including historical changes. Capture founders, share percentages, director appointments, registration address, and authorized capital. Our Russian Company Checker automates the initial pull.

- For Cyprus parents: the Department of Registrar of Companies (DRCOR) annual returns list shareholders and beneficial owners (post-2021 BO register, with caveats below).

- For UAE: NES (National Economic Register) public extracts and free-zone licensing portals (DIFC, ADGM, JAFZA) where they expose shareholder data.

- For BVI / Cayman / Marshall Islands: company registries are largely closed; rely on leaked datasets (Pandora Papers, Paradise Papers) via ICIJ's Offshore Leaks Database and OCCRP Aleph.

- For Kazakhstan: stat.gov.kz and kgd.gov.kz for tax registration and ownership data.

Step 2 — Cross-reference against sanctions and PEP datasets

- Run every named natural person and entity through OpenSanctions (opensanctions.org), which consolidates OFAC SDN, EU Consolidated List, UK OFSI, UN Security Council, and over 200 other lists.

- Cross-check against OCCRP Aleph for leak data, court filings, and journalism archives.

- For PEP exposure, the OpenSanctions PEP dataset and Wikidata's politician schema are the public baselines.

- Our Sanctions Check tool performs this multi-list match in one query.

Step 3 — Identify the structural patterns

- Sum ownership across all named natural persons. If two or more individuals each hold 24–49% and share a surname, address, or known business association, treat the structure as a possible aggregation case requiring further investigation.

- Look for trust or foundation interposition between the operating entity and the natural-person beneficiaries. Note the jurisdiction; certain jurisdictions (Liechtenstein Anstalt, Cyprus International Trust) are over-represented in evasion structures.

- Map the corporate-services provider. If the registered agent or director also appears on entities linked to designated persons, document the proximity.

- Check for pre-designation ownership transfers, especially to family members. Russian EGRUL historical extracts make this trivial within Russia; Cyprus and offshore transfers require leak-database cross-reference.

Step 4 — Add the control overlay (post-GVA)

- Identify signatories on bank accounts where disclosed (court filings, regulatory disclosures).

- Map board composition and check directors against known associate networks — LinkedIn, prior appointments in EGRUL, Pandora Papers director lists.

- Identify management contracts, voting trusts, and shareholder agreements where any have been disclosed (e.g., as exhibits in litigation).

- Document fund-flow patterns from any available source — SEC filings, court exhibits, leaked banking data — that suggest economic benefit accruing to a person not formally on the cap table.

Step 5 — Document the analytic chain

- Every assertion in the final memo must be sourced to a primary record with a retrievable URL or document identifier.

- Distinguish explicitly between direct evidence (e.g., a registry extract showing a 49% holding), inference (e.g., shared address between two entities suggests common control), and unknowns (e.g., trust deed not available).

- Conclude with a confidence rating. We use a four-tier scale: confirmed / probable / possible / unsupported. Counsel and compliance officers need the analyst's calibration, not just the underlying facts.

Limitations and caveats

This methodology has gaps. Acknowledging them is part of the analysis.

- Closed registries. BVI, Cayman, Marshall Islands, Nevis, and several U.S. states (Delaware, Wyoming, Nevada) do not publish beneficial ownership. The U.S. Corporate Transparency Act's beneficial ownership reporting regime, as of the date of this briefing, has been substantially narrowed in scope and is not a counterparty-accessible source. For these jurisdictions, the analyst is dependent on leak databases — which means ownership states post-2021 (the Pandora Papers cut-off) are increasingly stale.

- Trust opacity. Trust deeds are private in every major trust jurisdiction. Without them, the analyst cannot verify whether a settlor retains beneficial ownership. This is the structural reason Heritage Trust evaded automatic blocking for four years.

- Cyprus BO register caveats. The Cyprus beneficial ownership register, mandated by the EU's 5th AML Directive, was made publicly accessible in 2021. The Court of Justice of the EU's November 2022 judgment in WM and Sovim SA (Joined Cases C‑37/20 and C‑601/20) invalidated the public-access provision; access has since been restricted to legitimate-interest applicants in most Member States. This materially reduces what is open-source available in 2026 versus 2021.

- Russian registry restrictions. Since 2022, certain categories of Russian companies (notably defense-sector and sanctioned entities) have been permitted to redact founder and director information from public EGRUL extracts. The base layer of our methodology has degraded since the start of the war.

- Inference is not proof. A shared address, a common director, or a temporal correlation between a designation and a transfer is not evidence of evasion. It is a lead. The methodology produces an evidence map; legal conclusions belong to counsel.

What compliance teams should actually do

Five concrete steps that emerge from the documented cases:

- Treat every Russian-nexus counterparty as requiring an ownership reconstruction, not a name screen. Automated screening produces a green light on every entity that has been engineered to sit below the threshold. The Heritage Trust structure passed every name screen for over four years.

- Document the 50% calculation. If your screening conclusion is "no aggregate blocked ownership," your file should show the calculation: every named owner, the source of each ownership figure, and the date of the source. If you cannot produce the calculation, you have not done the screening.

- Treat 40–49.99% as a flag, not a clearance. The Deripaska 44.95% and the GVA Capital enforcement establish that ownership immediately below the threshold is itself a structural indicator. Files with sub-50% ownership by sanctioned-adjacent persons should trigger control analysis, not file closure.

- Map control, not only ownership. Post-GVA, knowledge that a sanctioned person retains beneficial interest or exerts control over assets is a sufficient basis for blocking-property obligations even where the 50% formal threshold is not met. Compliance files should reflect this.

- Rebuild the file when sanctions evolve. A counterparty cleared in 2021 against a 2021 ownership structure is not cleared in 2026. Designations of family members, restructurings, and intra-family transfers all change the calculation. Periodic re-screening is not optional.

Methodology references: OFAC 50-Percent Rule plain-English explainer · OFAC General Licenses · CASP under MiCA. Try our 50-Percent-Rule calculator to compute aggregate sanctioned ownership across multi-tier corporate chains.

Methodology disclosure

This briefing relies exclusively on public sources. We did not access any leaked private data not already published by ICIJ, OCCRP, or other journalistic consortia. The case discussions reflect facts as stated in U.S. Treasury press releases, OFAC FAQs, EN+ Group public disclosures, court filings cited in media coverage, and reporting by ICIJ and partners. Where we have characterised structural patterns, we have done so by inference from the public record and have flagged the inference as such.

We do not name individuals, entities, or transactions that are not already in the public record. Where an inference is contested or unverifiable, we have said so in the body of the text.

Sources and further reading

- OFAC FAQ 401 — The 50 Percent Rule. U.S. Department of the Treasury, Office of Foreign Assets Control.

- U.S. Treasury Blocks Over $1 Billion in Suleiman Kerimov Trust. Press release JY0841, 30 June 2022.

- OFAC FAQs 398–402 — Entities Owned by Blocked Persons.

- OFAC FAQ 402 — Divestment.

- A Breakdown of the Sanctions Deal between the United States and Oleg Deripaska. Atlantic Council.

- Deripaska, EN+, and Rusal: A Split Decision with Implications for U.S. Sanctions. German Marshall Fund / Joshua Kirschenbaum.

- OFAC Announces Intent to Remove Sanctions on UC Rusal plc, En+ Group plc, and JSC EuroSibEnergo. K&L Gates legal alert, January 2019.

- Treasury blocks $1 billion in Delaware trust tied to Russian oligarch. CNN, 30 June 2022.

- ICIJ reveals more than 800 Russians behind secret companies. International Consortium of Investigative Journalists.

- Suleyman Kerimov — biographical profile. Wikipedia, citing Russian and English-language press reporting.

- OFAC Imposes Large Russia Penalties as 2025 Comes to a Close. Lexology / law-firm commentary.

- Recent OFAC and DOJ Activity Signals Potential New Era of Control-Based Sanctions Enforcement. King & Spalding.

- OFAC Compliance: Legal Framework, Enforcement Risks, and 2024–2025 Enforcement Developments. National Law Review.

- Pandora Papers investigation index. ICIJ. See in particular reporting on Demetriades LLC and Alcogal.

- Pandora Papers: An offshore data tsunami. ICIJ. Dataset overview.

- OpenSanctions consolidated sanctions dataset.

- OCCRP Aleph — investigative dataset platform.

- ICIJ Offshore Leaks Database.

Need an ownership reconstruction on a sanctions-adjacent counterparty?

We perform forensic UBO analysis using the methodology in this briefing — multi-jurisdictional registry extracts, leak-database cross-reference, control mapping, and documented evidence chains with confidence ratings. Deliverables are written to be read by counsel.

Request an Investigation