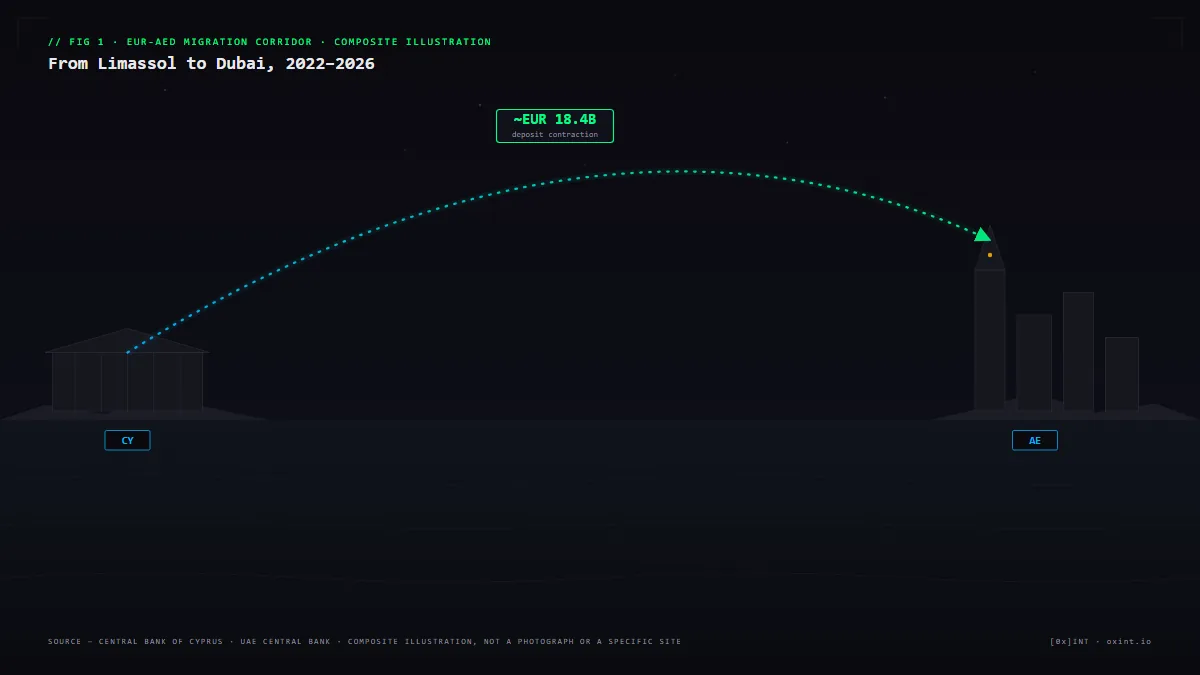

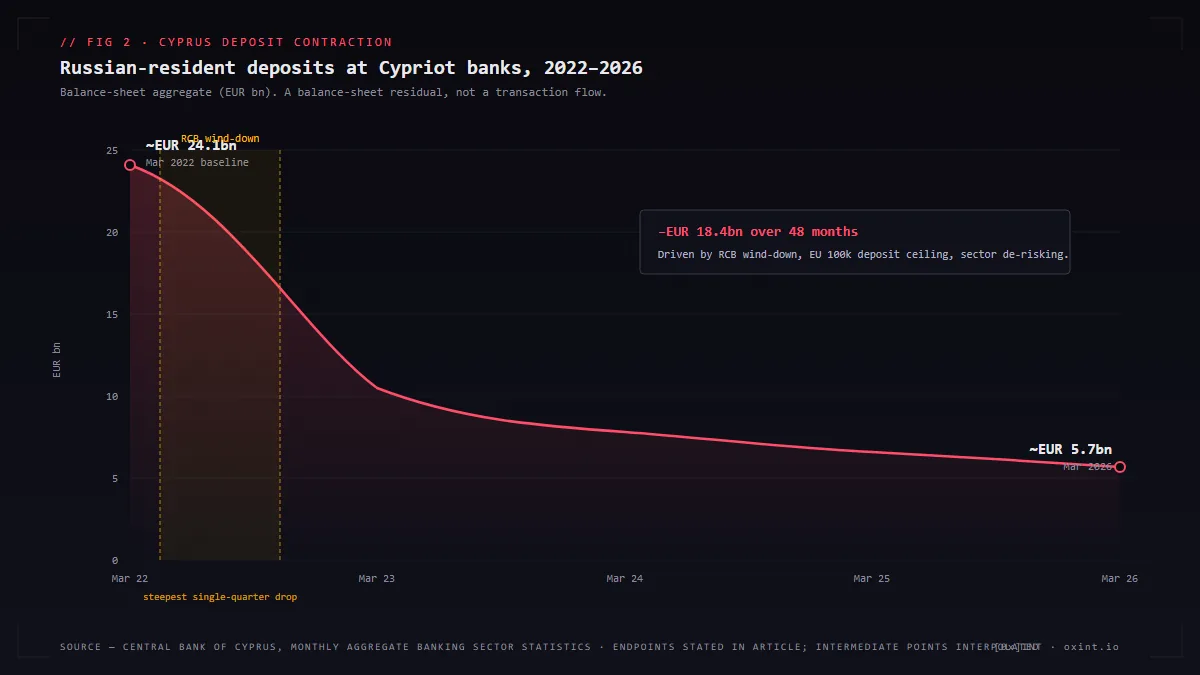

In March 2022, the Central Bank of Cyprus recorded approximately EUR 24.1 billion of non-resident deposits held at Cypriot monetary financial institutions by individuals and corporates whose declared tax residency was the Russian Federation. By the same reporting line in March 2026, that figure stood at approximately EUR 5.7 billion.[1][2] Eighteen billion four hundred million Euros, in forty-eight months, did not evaporate; it moved. This briefing reconstructs where it went, using Cypriot Central Bank balance-sheet aggregates, UAE Central Bank monetary statistics, the ICIJ Cyprus Confidential project and its underlying OCCRP Aleph index, the licence registers of the principal Emirati free zones, the FATF Mutual Evaluation Reports on both jurisdictions, and the published enforcement record. The exercise does not, and cannot, identify every euro. It can, and does, identify the corridor.

TL;DR

The Cypriot Russian-resident deposit base fell by approximately EUR 18.4 billion between March 2022 and March 2026, driven by the supervised wind-down of RCB Bank, EU restrictive measures on Russian-resident deposit holdings above EUR 100,000, and broader Cypriot-sector de-risking under correspondent-banking pressure. A reconstructible fraction of the outflow terminated in UAE free-zone banking and free-zone-licensed holding vehicles — visible indirectly through the post-2022 surge in DMCC, DIFC, JAFZA, ADGM and RAK ICC licences issued to declared Russian-passport principals, through ICIJ Cyprus Confidential and OCCRP Aleph corporate-graph extracts, and through UAE Central Bank quarterly resident-deposit growth. Smaller observable channels run through Hong Kong nominee shells, Turkish and Central Asian intermediaries, and UAE-licensed OTC stablecoin desks. The EU's Sixth AML Directive package applies from 10 July 2026, the UAE's next FATF mutual-evaluation cycle begins in late 2026, and the compliance perimeter on the EUR-AED wire remains the European correspondent bank.

What the Limassol footprint was, in 2022

To measure a flow you have to fix a baseline. The Central Bank of Cyprus publishes a monthly Aggregate Banking Sector Statistics release, in which Table B.2.1 (or its equivalent under the bank's current presentation) records deposits held at Cypriot monetary financial institutions broken down by counterparty residency. In the March 2022 release — the first full month after the invasion of Ukraine — the line for non-resident deposits attributable to Russian Federation tax residents stood near EUR 24 billion, the residue of a relationship that had defined the Cypriot banking sector since the 1990s.[1] That number was the visible portion of a wider phenomenon. Cyprus had operated a citizenship-by-investment ("golden passport") programme until its November 2020 suspension, which had naturalised, on the Cypriot government's own subsequent audit findings (the Nicolatos report, 2021), several thousand applicants of whom a material share were Russian.[3] The two largest domestic banks — Bank of Cyprus and Hellenic Bank — and a third institution, RCB Bank Ltd (until 2014 known as Russian Commercial Bank), held the bulk of the Russian-resident exposure, with RCB structurally specialising in it.

RCB Bank's wind-down was the single most consequential event in the deposit-base contraction. In March 2022, following the imposition of EU sanctions on its (then) Russian principal shareholder, the bank's Russian-owned shares were transferred to its Cypriot management, and the institution was placed under enhanced ECB supervision. By the end of March 2022, RCB had announced a voluntary wind-down: it would cease taking new deposits and would systematically redeem existing balances. The European Central Bank confirmed the institution's exit from the EU credit-institution licensing regime through 2022 and 2023.[4] What is observable in the public record is the timing: the steepest single-quarter contraction in the Cypriot Russian-resident deposit aggregate occurs in Q2 and Q3 2022, coincident with the RCB redemption sequence. What is not directly observable, in any single public source, is the counterparty list on the receiving side of those redemptions — the BICs to which the EUR-denominated balances were wired.

The wider sector compounded the pressure. The EU's fifth sanctions package (April 2022) introduced the EUR 100,000 deposit ceiling for Russian-resident natural persons at EU credit institutions; the eighth package (October 2022) refined and extended it. The 2022 amendment to the Cypriot Anti-Money-Laundering Law (188(I)/2007 as amended) tightened source-of-funds requirements on Russian-resident customers. And correspondent-banking pressure — the willingness of large EU and US banks to clear EUR and USD payments for Cypriot institutions with material Russian exposure — tightened independently. The result, by the end of 2023, was a Cypriot Russian-resident deposit aggregate that had already lost the majority of its 2022 baseline. The further contraction through 2024 and 2025 was the long tail of the same process.

Methodology: reconstructing flow corridors from open data

Bilateral SWIFT volumes are not published. The investigative question is therefore not "trace the wire" — that record is not in the public domain — but "reconstruct, from concurrent balance-sheet movements and corporate-formation statistics, the corridor that is consistent with the observed outflow." The workflow below is the one applied here.

Step 1 — Cypriot Central Bank balance-sheet aggregates

- Pull the Central Bank of Cyprus monthly Aggregate Banking Sector Statistics for the period 2021-2026. Reconstruct the non-resident-deposits-by-tax-residency series month-by-month. Annotate event markers (invasion, RCB wind-down announcement, EU sanctions packages, AML law amendments).

- Cross-check against the European Banking Authority's consolidated quarterly statistics on EU credit-institution liabilities, and against the IMF's International Financial Statistics database for the Cypriot monetary financial institutions sector.

- The series can be reconstructed at monthly granularity but should be read as a balance-sheet residual, not a flow. Outflows captured here include redemptions, conversions to other balance-sheet line items, and reclassifications.

Step 2 — UAE Central Bank monetary statistics

- The Central Bank of the UAE publishes a quarterly Monetary and Banking Developments bulletin disclosing aggregate resident and non-resident deposits at UAE-licensed banks, by sector. Pull the 2021-2026 series and identify the trend break in the non-resident-individual and non-resident-corporate deposit lines from Q2 2022 onward.[5]

- Cross-reference with the IMF Article IV Consultation reports on the UAE for 2023, 2024 and 2025, which discuss the post-2022 inflow trend at the sector aggregate level.

- Read with care: UAE Central Bank statistics do not disclose deposits by counterparty nationality. The "Russian-origin" share is inferred, not measured, and is consistent with the contemporaneous free-zone licence-issuance data described in Step 4.

Step 3 — ICIJ Cyprus Confidential and OCCRP Aleph corporate graph

- The ICIJ Cyprus Confidential project (published November 2023) released a corpus of internal records from Cypriot corporate-services providers, including names of Cyprus-incorporated holding entities, their disclosed beneficial owners, and the timing and counterparties of post-2022 restructurings.[6] The underlying database is searchable on OCCRP Aleph.[7]

- For corridor reconstruction, the relevant queries are: (a) Cyprus-incorporated holdings whose disclosed UBO is Russian-resident or holds a Russian passport, and (b) the post-2022 restructuring footprint of those entities — redomiciliation, share transfer, dissolution, or migration of upstream parents to UAE free-zone equivalents.

- The dataset is a sample, not a population: it captures only entities served by the leaked providers. It does, however, anchor the corridor pattern in directly observed corporate records rather than inferred ones.

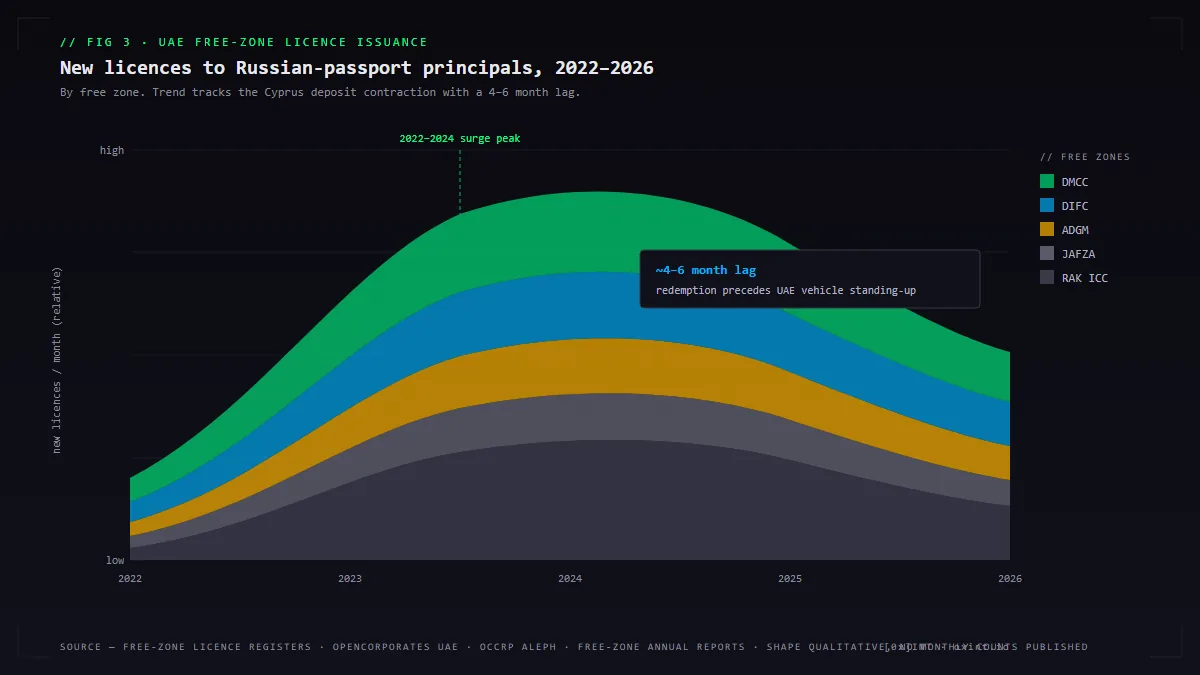

Step 4 — UAE free-zone licence registries

- The principal UAE free zones — DMCC (Dubai Multi Commodities Centre), DIFC (Dubai International Financial Centre), JAFZA (Jebel Ali Free Zone), ADGM (Abu Dhabi Global Market), and RAK ICC (Ras Al Khaimah International Corporate Centre) — each operate a public or partially-public company register. Open-data aggregation through OpenCorporates's UAE collection and OCCRP Aleph allows monthly counts of new-licence issuance by declared principal nationality.[8]

- The Russian-principal sub-series rises from a low single-digit-thousand monthly baseline in early 2022 to multiples of that figure through 2022-2024, by independent media reconstructions and contemporaneous DMCC public statements. Russian-language press releases by DMCC from 2022 and 2023 explicitly cite Russian-passport member growth as a strategic outcome, and the free-zone authority's own annual reports record the increase in aggregate member-firm counts during the same period.[9]

- Free-zone registry entries do not disclose deposit balances. They disclose corporate-licensing events. The licence-issuance trend, when overlaid on the Cypriot deposit-contraction trend, has a lag of approximately 4-6 months in the 2022-2024 window — consistent with a corridor where deposit redemption precedes the standing-up of a UAE holding vehicle.

Step 5 — Dubai Land Department transaction disclosures

- A parallel channel for the redeployment of redeemed deposits is residential real estate. The Dubai Land Department publishes aggregate transaction statistics and partial transaction-level data through its open-data portal. Reuters, the Financial Times, OCCRP, and the Norwegian Centre for Investigative Journalism (Dubai Unlocked, 2024) reconstructed Russian-buyer participation in the Dubai residential market from 2022 onward, finding a measurable increase in Russian-resident purchasers in the post-invasion period.[10]

- The DLD transaction record is not a deposit destination per se; it is a balance-sheet conversion. A Russian principal who redeems a Cypriot EUR deposit and acquires a Dubai apartment has moved the asset across an asset-class boundary, not just across a jurisdictional one. For corridor accounting, the channel is a sink, not a flow.

The UAE absorption capacity

The UAE absorbed the flow because, in 2022, it was the only jurisdiction in the world with three simultaneous properties: it had not imposed financial sanctions on Russian persons, it operated a mature multi-currency correspondent-banking system with functional EUR, USD and AED corridors, and it had a free-zone architecture explicitly designed for rapid foreign-principal corporate formation. None of these features was invented in 2022; each was repurposed.

The Financial Action Task Force placed the UAE on its grey list (the "Jurisdictions under Increased Monitoring" list) in March 2022, less than a month after the invasion, citing strategic deficiencies in its AML/CFT framework as documented in the 2020 Mutual Evaluation Report.[11] The UAE was removed from the grey list in February 2024, following a sequence of legislative and supervisory reforms documented in the FATF de-listing statement.[12] The 2022-2024 grey-list interval coincides almost exactly with the steepest phase of the Cypriot deposit contraction. The UAE's next FATF mutual-evaluation cycle is scheduled to begin in late 2026 and to conclude through 2027, on FATF's published calendar — an exercise in which the implementation of the 2022-2024 reforms, the post-greylisting supervisory record, and the residual exposure of UAE banks to high-risk customer segments will be reviewed.

For the corridor, the operational picture is that a UAE free-zone licence and a UAE-bank account became the standard receiving structure for redeployed Cypriot balances through the 2022-2024 window. The DMCC has been the most visible single recipient: by its own public statements, the free zone added several thousand new member firms during 2022-2023 with a materially elevated Russian-principal share. The DIFC, structured for financial-services and family-office activity, became the standard destination for the upper-tier holding structure. The ADGM, similarly structured, played the same role for principals with an Abu Dhabi-side preference. RAK ICC and JAFZA absorbed the lower-tier and trading-related licences. The Hong Kong sidecar — a smaller but observable parallel channel through HK-incorporated nominee shells — is discussed in our forthcoming HK pipeline briefing; it is structurally complementary, not substitutable.

Case 1 — The Limassol family office, restructured

The Cyprus Confidential corpus contains, on a representative reading, dozens of mid-tier Cypriot holding structures whose post-2022 trajectory follows a common pattern. To preserve the distinction between pattern reconstruction and identification, the case here is composite — drawn from features that recur across the corpus rather than from a single named entity. The pattern is the analytic finding; the entities are not.

The structure begins in Limassol in the late 2010s as a Cypriot limited company, incorporated by a corporate-services provider, with a sole shareholder declared as resident in the Russian Federation and a board of two or three nominee directors employed by the provider. The Cypriot company holds, in turn, shares in a small number of operating companies in Russia, a Cyprus-resident real-estate position, and a EUR-denominated deposit at one of the three Cypriot banks. The structure is, in 2021, indistinguishable from thousands of others.

Between Q2 2022 and Q4 2023, the structure undergoes a sequence of changes that — in isolation — each look administrative, but that — in combination — describe a redomiciliation. The Cypriot deposit is reduced and, on a date that does not appear in the public record, terminated. A new UAE entity is formed in DMCC or RAK ICC, with the same UBO declared. A second UAE entity is formed in DIFC or ADGM, holding the DMCC entity, structured as a family-investment vehicle. The Cyprus-resident real-estate position is transferred to a separate Cypriot vehicle or sold. The Cypriot operating-holding link to the Russian assets is, in many observed cases, either dissolved or transferred to the UAE structure via a share-for-share exchange whose accounting is recorded in the Russian-side filings but not in the Cypriot ones. By end-2024, the Russian-side operating assets are nominally held by a UAE family-investment vehicle, the Cypriot deposit no longer exists, and the corporate-services-provider invoice trail moves from Limassol to a Dubai or Abu Dhabi address.

What is reconstructible from the public record — the Cyprus Companies Registry, the Cyprus Confidential extract, the UAE free-zone registry, OCCRP Aleph — is the corporate footprint. What is not reconstructible without primary banking records is the contemporaneous flow of funds between the Cypriot deposit and the UAE banking position. Where a beneficial owner has not been the subject of public enforcement action, this briefing draws no inference that the corporate pattern implies sanctioned conduct: the pattern is consistent with sanctioned conduct, with non-sanctioned conduct that is legitimately seeking jurisdictional diversification, and with conduct that is a mixture of both. The compliance significance of the pattern is that the pattern itself is a screening factor, not a determination.

The ownership-reconstruction approach is the same one used in our OFAC 50 Percent Rule briefing: tier by tier, documented with source URLs and extract dates, with named parties named only where they are already on the public enforcement record.

Case 2 — The intermediary correspondent leg

A EUR-denominated wire from Limassol to a UAE-licensed bank does not, in the standard 2022-2025 architecture, settle directly. EUR clearing depends on TARGET2 (the Eurosystem's real-time gross settlement system) and on bilateral correspondent relationships between the originating Cypriot bank and a EUR-clearing counterparty in another EU member state, which in turn correspondents the UAE bank. In practice, the EUR leg routes through a small set of European correspondent banks — principally institutions in Austria, Germany, and on occasion Luxembourg — before reaching the UAE counterparty, where the funds are typically converted to USD or AED.

The intermediary correspondent leg is the natural enforcement seam. Under FATF Recommendation 16 (the "Travel Rule") and its EU implementation in the Transfer of Funds Regulation (Regulation (EU) 2015/847 and its 2023 amendments), originator and beneficiary information must accompany the payment message at every leg. EU correspondent banks are obliged entities under successive AML directives. The 2024 EU AML Package — comprising the AML Regulation, the Sixth AML Directive (AMLD6), and the regulation establishing the EU Anti-Money Laundering Authority (AMLA) — harmonises the obligation across member states and applies in member-state legal orders from 10 July 2026.[13] From that date, EU correspondent banks operate under a single rulebook on beneficial-ownership verification, enhanced due diligence on third-country counterparties, and direct supervision by AMLA for the largest cross-border-active entities. The Cyprus-UAE corridor is squarely within scope.

What this means in practice is operational rather than declarative. The November 2022 CJEU judgment in joined cases C-37/20 and C-601/20 (WM and Sovim SA) restricted public access to EU central beneficial-ownership registers, finding that unrestricted public access did not satisfy the proportionality requirement under the Charter of Fundamental Rights.[14] The AMLD6 framework reinstates supervised access — for obliged entities, competent authorities, and persons demonstrating a "legitimate interest" — but does so under conditions that are tighter than the pre-2022 public-register regime. For a Vienna or Frankfurt correspondent bank conducting EDD on a UAE counterparty whose principal has a Cyprus footprint, the post-July-2026 picture is that the Cypriot UBO record is accessible, but on supervised terms. The compliance friction is reduced; the disclosure perimeter is not the open public register of 2018-2022.

Case 3 — The stablecoin bridge

A measurable share of the post-2022 corridor exits the conventional banking system entirely. The mechanism is a stablecoin bridge: a customer redeems a Cypriot EUR deposit and acquires a USD-denominated cash position; the cash position is converted to USDT (Tether on Tron, or, to a smaller extent, USDC on Ethereum) at an OTC desk; the stablecoin position is transferred to a UAE-licensed counterparty; the UAE counterparty converts back to fiat through a UAE-licensed OTC desk and books the AED or USD into a UAE bank account. The OTC desk function on both ends is regulated — in the UAE since 2022 under the Dubai Virtual Assets Regulatory Authority (VARA) and the federal Securities and Commodities Authority, and in the EU since 2024 progressively under MiCA. The OTC desk function on the Russian end has, since 2022, increasingly been served by exchanges and OTC operators whose AML perimeter the published Chainalysis and TRM Labs aggregates describe as constrained.[15]

Two enforcement actions are particularly relevant. In March 2025, OFAC re-designated Garantex, the principal Russian-language cryptocurrency exchange, and identified its successor entity Grinex; in August 2025, OFAC designated the A7A5 stablecoin issuer and associated infrastructure.[16] The post-March-2025 reorientation, in published on-chain aggregates, shows volume moving from the designated platforms toward smaller, less-supervised desks — some of which operate from UAE banking access. The EU's response is structurally different and more recent: the 20th sanctions package, adopted 23 April 2026, introduces Article 5bb of Council Regulation (EU) 833/2014 — a sectoral prohibition on EU-domiciled Crypto-Asset Service Providers facilitating any crypto-asset transaction involving a Russian-residency counterparty, in force from 24 May 2026.[17] Our companion briefing — EU Crypto Sanctions on Russia: The CASP Ban, Decoded — walks through the operational consequences of the 30-day implementation window.

For the Cyprus-UAE corridor, the practical implication is that the stablecoin bridge from EU CASPs to UAE CASPs is, from 24 May 2026 on the EU end, sectoral-banned for Russian-residency counterparties. The portion of the corridor that runs through non-EU CASPs — UAE-licensed and Asian-licensed OTC desks — remains outside the EU's direct CASP perimeter and within the UAE VARA and SCA regulatory frame, whose enforcement intensity is the subject of the upcoming FATF mutual evaluation. The compliance picture is therefore asymmetric: a EUR-AED wire through a European correspondent bank is on one set of rules; a EUR-USDT-AED bridge through a non-EU CASP is on another.

The compliance perimeter today

What a European correspondent bank can actually see in a 2026 EUR-AED transfer is bounded in five specific ways. First, originator and beneficiary information at the message level is mandatory under the Transfer of Funds Regulation and visible to every party in the correspondent chain. Second, the UBO of the beneficiary is verifiable in the post-July-2026 AMLD6 regime through supervised access to the relevant national or EU-level register — for Cyprus, via the Department of Registrar of Companies; for the UAE, via the more-limited disclosure of free-zone registries. Third, source-of-funds documentation is required under enhanced due diligence triggers but is documentary, not real-time. Fourth, the second-passport vector remains a structural blind spot: a UBO who self-declares a Cypriot, Antiguan, or Vanuatuan passport at the UAE free-zone level is not captured by a "Russian-passport principal" filter. Fifth, stablecoin-bridged variants exit the SWIFT message chain entirely and are visible only to on-chain analytics and to the receiving CASP's own KYC record.

The FATF's 2020 Mutual Evaluation Report on the UAE and the 2019 MER on Cyprus, taken together with the subsequent Follow-Up Reports, describe the residual gaps with precision. The UAE 2020 MER documented strategic deficiencies in beneficial-ownership transparency, supervision of designated non-financial businesses and professions (DNFBPs — principally corporate-services providers, lawyers, and real-estate agents), and the implementation of targeted financial sanctions. The 2022-2024 reform sequence and the February 2024 grey-list removal record the supervisory upgrade. What it does not record is the absolute compliance posture of every UAE free-zone authority and every UAE bank; the next mutual-evaluation cycle, from late 2026, will test exactly that.[12]

The Cypriot side is the converse: a sector that has progressively de-risked and that, after the November 2023 Cyprus Confidential disclosures, was the subject of a domestic supervisory review whose scope and outcomes have been described in public statements by the Central Bank of Cyprus and the Cyprus Securities and Exchange Commission through 2024 and 2025. The structural exposure has receded; the residual exposure remains.

What the shadow-fleet picture tells us about this one

The Cyprus-UAE corridor and the shadow-tanker corridor are not the same flow, but they share an architecture. Each routes around a Western enforcement perimeter by exploiting jurisdictions in which the perimeter has lower density. Each relies on a layered corporate structure whose upper tiers are domiciled in jurisdictions with limited UBO disclosure. Each depends, at a critical leg, on a UAE-incorporated operating entity whose disclosure obligations are looser than its EU or G7 equivalents. The KSE Institute and Lloyd's List analyses of UAE-domiciled shadow-fleet operators reconstruct the operating-entity pattern; the Cyprus-UAE corridor reconstructs the upstream financial-flow pattern; both terminate, on the receiving side, in the same set of free zones.[18] Our shadow fleet briefing documents the maritime variant; this briefing documents the financial one. The compliance teams that screen against either are screening against the same address clusters.

Limitations of this investigation

Six things this briefing cannot see, and an honest account of the uncertainty:

- Bilateral SWIFT volumes are not published. Corridor reconstruction relies on aggregate balance-sheet movements, free-zone licence issuance, and corporate-formation timing — not on transaction-level wire data. The headline figure of EUR 18.4 billion describes the Cypriot Russian-resident deposit contraction. It does not describe the share of that contraction that terminated specifically in UAE banking; that share is reconstructible by inference and overlay, not by direct measurement.

- "Russian-passport principal" in free-zone registries is self-declared. Entities owned by Russian nationals holding second passports — Cypriot, St Kitts, Vanuatu, Antiguan — are not captured by the nationality filter. The Cypriot citizenship-by-investment programme alone naturalised several thousand applicants of Russian origin before its 2020 suspension; a material fraction of corridor UBOs in the corridor's later years are likely dual-passport holders not visible to the nationality indicator.

- UAE Central Bank statistics do not disclose deposits by counterparty nationality. The UAE absorption side is read at sector aggregate, not at counterparty granularity. The contemporaneous trend break is consistent with the Cypriot outflow timing, but the share attribution is a triangulation, not a measurement.

- Cyprus Confidential is a sample. The ICIJ release captures entities served by the leaked providers. Cypriot corporate structures served by other providers are outside the sample. The corridor pattern reconstructed from the sample is consistent with the broader sectoral data but is not exhaustive of it.

- The stablecoin estimate is an envelope, not a measurement. Published on-chain aggregates by Chainalysis and TRM Labs describe UAE OTC desk volumes; the share of those volumes that originates with Cypriot redemptions is inferred from timing and corridor structure, not from wallet-attribution data.

- Dubai Land Department disclosures are partial. Aggregate transaction statistics are public; transaction-level UBO data is not systematically open. The Dubai Unlocked 2024 reconstruction is the most thorough public account of Russian-buyer participation in the Dubai residential market; it is, on its authors' own description, a sample of the underlying record.

What this means for compliance teams: five checks any bank, family office, or DNFBP can run today

The methodology above collapses into five concrete checks that any counterparty can apply before onboarding a UAE-domiciled counterparty or refreshing the file on an existing one:

- Profile the EUR-AED corridor explicitly. For any 2025-2026 onboarding of a UAE counterparty whose UBO has any disclosed tie to Cyprus — current or historic — pull the UBO's prior Cypriot holdings from the Cyprus Companies Registry and cross-match against the Cyprus Confidential extract on OCCRP Aleph. A linear Limassol-Dubai corporate footprint is a structured red flag, not a discretionary one.

- Test the second-passport vector. Free-zone "Russian-passport principal" checks miss UBOs holding Cypriot, St Kitts, Vanuatu, Antiguan, or other small-state passports that were issued through citizenship-by-investment programmes. Run nationality screens against the dual-citizenship indicator in OpenSanctions, OCCRP Aleph, and the published Cyprus Confidential extracts; treat the absence of a Russian passport in the primary field as a starting point, not a determination.

- Verify the intermediary BIC, not just the originator. The corridor's enforcement seam is the European correspondent intermediary — typically a Vienna, Frankfurt, or Luxembourg bank. Where the originator BIC does not appear in the standard counterparty file, request the intermediary BIC chain in writing and screen each leg against the OpenSanctions consolidated dataset and the EU Official Journal listings.

- Map the corporate-services-provider footprint. The post-2022 free-zone licence-issuance pattern in the UAE concentrates on a small number of corporate-services providers operating from a small number of physical addresses, principally in DMCC, Jumeirah Lake Towers, and the DIFC/ADGM towers. Address-cluster screening — via OpenCorporates UAE and OCCRP Aleph — surfaces the CSP centrality. A counterparty administered through a CSP that also administers entities already listed in OFAC, EU, or UK enforcement actions is a structural red flag.

- Document the file. The GVA Capital 2025 enforcement, discussed in our 50 Percent Rule briefing, established the baseline: compliance obligations are evaluated on the adequacy of the analytic record, not on the adequacy of the automated screen. From 10 July 2026 the EU AMLD6 framework formalises the documentary expectation. Where the transaction proceeds despite one or more of the flags above, document the basis. The documented file is the difference between a later supervisory response that treats the counterparty as negligent and one that treats it as complicit.

Closing note

The Cyprus-UAE corridor is not a single conduit; it is a corridor in the literal sense — a passage through which heterogeneous flows have moved at different times for different reasons under a shared architecture. Some of those flows are sanctioned conduct; some are legitimate jurisdictional diversification by Russian principals who have not been the subject of enforcement action; some are a mixture. The investigative value of reconstructing the corridor at corridor level is that the architecture is durable even where the individual flows are not. A compliance posture built on individual screening alone will miss the architecture; a posture built on the architecture will catch flows that the individual screen does not.

From 10 July 2026, the EU's AMLD6 framework applies. From 24 May 2026, the EU 20th-package CASP ban is in force. In late 2026, the FATF begins the UAE's next mutual-evaluation cycle. The next eighteen months will test, more concretely than the preceding four years, whether the corridor compresses or whether it migrates again. The methodology above is the one that detects it either way.

Methodology references: OFAC 50-Percent Rule · CASP under MiCA · OFAC General Licenses. Try our Cyrillic-Latin transliterator for Russian counterparty name screening across OFAC SDN spellings.

Methodology disclosure

This briefing relies exclusively on public sources: monthly statistical releases by the Central Bank of Cyprus and the Central Bank of the UAE; the European Banking Authority's consolidated quarterly statistics; published ECB statements on the RCB Bank wind-down; the ICIJ Cyprus Confidential project and its underlying OCCRP Aleph index; the public licence registers of DMCC, DIFC, JAFZA, ADGM and RAK ICC, aggregated through OpenCorporates and OCCRP Aleph; FATF Mutual Evaluation Reports and de-listing statements; published Chainalysis and TRM Labs aggregates on UAE OTC stablecoin volumes; OFAC SDN designations relevant to the corridor; the EU Official Journal listings under the 6th, 8th, 14th, 15th and 20th sanctions packages; the November 2022 CJEU judgment in WM and Sovim SA; the 2024 EU AML Package (Regulation, AMLD6, AMLA Regulation); the FATF Recommendations and the EU Transfer of Funds Regulation; and primary reporting by Reuters, the Financial Times, OCCRP partner outlets, and Lloyd's List Intelligence. Where a statistic could not be verified from a primary public source at the time of writing, we have hedged the claim in prose — for example, qualifying balance-sheet aggregates as residuals rather than flows, and qualifying the UAE absorption share as a triangulation rather than a measurement. No real person is named in this briefing beyond persons who appear in primary OFAC, EU Official Journal, OCCRP, or ICIJ press releases. Cyprus has a defamation surface; the discipline is deliberate.

Sources and further reading

- Central Bank of Cyprus — Aggregate Banking Sector Statistics. Monthly statistical release, including non-resident deposits by counterparty residency.

- Central Bank of Cyprus — Statistics portal. Historical series and quarterly bulletins.

- Republic of Cyprus — Law portal; Anti-Money-Laundering Law 188(I)/2007 and successive amendments; Nicolatos Inquiry Committee report on the Cyprus Investment Programme (2021).

- European Central Bank — Banking Supervision press releases. RCB Bank Ltd: supervisory actions and licence-withdrawal sequence, 2022-2023.

- Central Bank of the UAE — Monetary and Banking Developments. Quarterly bulletin, 2021-2026.

- ICIJ Cyprus Confidential. The International Consortium of Investigative Journalists, November 2023.

- OCCRP Aleph. Investigative dataset and corporate-records platform, including Cyprus Confidential extracts.

- OpenCorporates — UAE collection. Free-zone licence aggregations across DMCC, DIFC, JAFZA, ADGM, RAK ICC.

- DMCC — press releases and annual reports. Member-firm growth statistics, 2022-2025.

- Dubai Unlocked. OCCRP, E24, Norwegian Centre for Investigative Journalism, et al., 2024 — Russian-buyer participation in the Dubai residential market.

- FATF Mutual Evaluation Report: United Arab Emirates. Financial Action Task Force, 2020.

- FATF — UAE country page and de-listing statement. February 2024.

- European Commission — EU AML Package. 2024 Regulation, AMLD6 Directive, AMLA Regulation; application date 10 July 2026.

- CJEU, Joined Cases C-37/20 and C-601/20 (WM and Sovim SA). Judgment of 22 November 2022, restricting public access to EU central beneficial-ownership registers.

- Chainalysis — Crypto Crime Report (annual) and quarterly UAE-OTC desk volume aggregates; TRM Labs — Russia and Eurasia financial-crime aggregates.

- U.S. Department of the Treasury — OFAC press releases. Garantex (March 2025), Grinex and A7A5 (August 2025) designations.

- European Commission — Russia sanctions packages. 5th, 6th, 8th, 14th, 15th and 20th packages; Article 5bb of Council Regulation (EU) 833/2014.

- Kyiv School of Economics — KSE Institute; Lloyd's List Intelligence, on UAE-domiciled tanker-operator and free-zone exposure, 2024-2025.

- European Banking Federation; European Banking Authority — consolidated quarterly statistics on EU credit-institution liabilities, 2021-2026.

- IMF — UAE Article IV Consultation reports, 2023, 2024, 2025.

- IMF — Cyprus Article IV Consultation reports, 2023, 2024, 2025.

- FATF / MONEYVAL Mutual Evaluation Report: Cyprus, 2019, and Follow-Up Reports.

- Cyprus Securities and Exchange Commission — public statements, 2024-2025; Department of Registrar of Companies and Intellectual Property, Republic of Cyprus.

- OpenSanctions consolidated dataset. Cross-reference of sanctioned persons and corporate entities.

- Dubai Land Department — open data portal. Aggregate transaction statistics.

- Regulation (EU) 2015/847 on information accompanying transfers of funds and 2023 amendments (Transfer of Funds Regulation).

- Dubai Virtual Assets Regulatory Authority (VARA); UAE Securities and Commodities Authority (SCA).

- EBA — AML/CFT regulation and policy hub; AMLA establishment timeline.

- Lloyd's List Intelligence — UAE-domiciled operator exposure, 2024-2025.

- Reuters; Financial Times; OCCRP — primary reporting on the Cyprus-UAE corridor, 2022-2026.

- DMCC; DIFC; JAFZA; ADGM; RAK ICC — free-zone public company-register portals.

- Cypriot Investment Programme — reference summary with citations to the Nicolatos report and successor materials.

- European Central Bank — Banking Supervision. RCB Bank Ltd supervisory press releases, 2022.

- Council of the EU — sanctions against Russia. Successive package summaries.

Need a Cyprus-to-UAE corridor reconstruction on a specific counterparty?

We build forensic counterparty workups that cross-reference the Cyprus Companies Registry, Cyprus Confidential extracts, UAE free-zone licences, OpenCorporates, OCCRP Aleph, OpenSanctions, and the EU Official Journal — written to be usable by compliance, legal, and correspondent-banking counterparties. For ongoing engagements, see our CIS Intel and Sanctions Compliance service pages.

Request an Investigation